Advertisement

How to Build an Emergency Fund From Scratch, Whatever Your Income

Four milestones that work whether you're saving ₹500 or ₹15,000 a month

A friend's laptop died two weeks before a client deadline. A replacement cost ₹42,000. She paid cash and moved on with her week. That's the entire point of an emergency fund — it turns a crisis into an inconvenience.

What Actually Counts as an Emergency

A medical bill, a job loss, an urgent repair, a family emergency — not a sale on a phone you wanted, not a wedding gift, not a "once in a lifetime" trip. If you can plan for it in advance, it belongs in a separate savings goal, not the emergency fund.

How Much You Actually Need

The common advice is 3-6 months of essential expenses — rent, groceries, utilities, EMIs, insurance. Adjust based on your situation: freelancers and single-income households should lean toward 6 months; salaried employees with a stable job and family backup can reasonably start at 3.

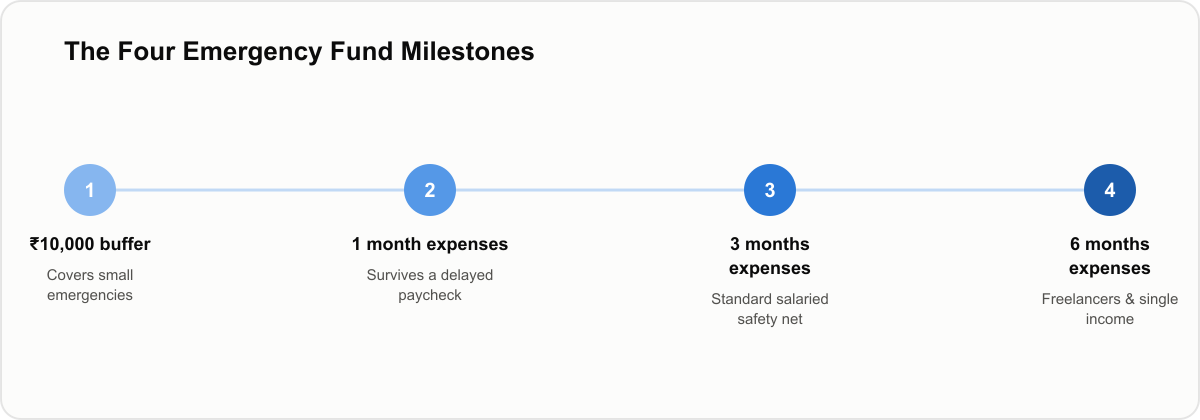

The Four Milestones

Milestone 1 — ₹10,000 buffer

This alone covers most small emergencies: a medical visit, an urgent repair, a month's rent shortfall. Build this first, before anything else, even before extra debt payments.

Milestone 2 — One month of expenses

Enough to survive a delayed paycheck or an unexpected month of reduced income without touching credit.

Milestone 3 — Three months of expenses

The standard safety net for a stable salaried job. Covers a job search that runs longer than expected.

Milestone 4 — Six months of expenses

Where freelancers, single-income households, and anyone in a volatile industry should aim to land.

Where to Actually Keep It

Liquid and boring: a separate savings account or a liquid mutual fund you can access within a day or two. Not stocks, not fixed deposits with a lock-in, not anything that can lose value or take a week to withdraw right when you need it most. The goal is availability, not returns.

Funding It on a Tight Budget

- Automate a fixed amount right after payday, even if it's ₹500 — automatic beats "whatever's left"

- Redirect one specific recurring expense (a subscription, a takeout order) directly into the fund

- Put windfalls — bonuses, tax refunds, gifts — straight into the fund before you get used to having the extra money

A Realistic Example

| Monthly savings | Time to Milestone 1 (₹10,000) | Time to Milestone 3 (3 months, ₹90,000 expenses) |

|---|---|---|

| ₹1,000/month | 10 months | ~7.5 years |

| ₹3,000/month | ~3.5 months | ~2.5 years |

| ₹5,000/month | 2 months | ~1.5 years |

The exact numbers matter less than the direction — Milestone 1 is achievable for almost anyone within a year, and it's the milestone that prevents most financial emergencies from turning into debt.

Where People Go Wrong

- Treating it as investment money — chasing returns on emergency savings defeats the purpose; you need it available, not growing

- Dipping into it for non-emergencies — a "great deal" isn't an emergency; redraw the line every time you're tempted

- Waiting to start until income is higher — ₹500 a month started today beats a "someday" plan for ₹5,000 a month

- Not replenishing after using it — treat a withdrawal as a temporary dip, not a permanent reset; rebuild it before resuming other savings goals

Questions Worth Answering

The Actual Point

An emergency fund isn't about the number in the account — it's about not having to make a bad decision (high-interest debt, selling an investment at a loss, borrowing from family) the day something goes wrong. Start with Milestone 1 this month.

Frequently Asked Questions

Advertisement

Was this article helpful?

Advertisement

Comments

No comments yet. Be the first to share your thoughts!

Related Posts

How to Save ₹1 Lakh in One Year on a ₹30,000 Salary

Earning ₹30,000 per month and want to save ₹1 lakh in a year? This practical guide shows exactly how to cut expenses and save more without feeling broke.

Zero-Based Budgeting: A Practical Guide to Giving Every Rupee a Job

The budgeting method that forces you to plan discretionary spending before you make it

Zero-based budgeting assigns every rupee of income a job before the month starts. A step-by-step method for setting one up, with a worked example.